|

70 |

|

FOMC Past Records:

Updates on 30 July 2020 Federal Reserve issues FOMC statement (released on 29 July 2020, 2:00 p.m. EDT) Extracts: The path of the economy will depend significantly on the course of the virus. The ongoing public health crisis will weigh heavily on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term. In light of these developments, the Committee decided to maintain the target range for the federal funds rate at 0 to 1/4 percent. The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals. …In determining the timing and size of future adjustments to the stance of monetary policy, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. To support the flow of credit to households and businesses, over coming months the Federal Reserve will increase its holdings of Treasury securities and agency residential and commercial mortgage-backed securities at least at the current pace to sustain smooth market functioning, thereby fostering effective transmission of monetary policy to broader financial conditions. In addition, the Open Market Desk will continue to offer large-scale overnight and term repurchase agreement operations. The Committee will closely monitor developments and is prepared to adjust its plans as appropriate.

Updates on 21 May 2020 Minutes of the Federal Open Market Committee, April 28-29, 2020 (released on 20 May 2020, 2pm EDT) Extracts: At the conclusion of the discussion, the Committee voted to authorize and direct the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the SOMA in accordance with the following domestic policy directive, for release at 2:00 p.m.: "Effective April 30, 2020, the Federal Open Market Committee directs the Desk to: •Undertake open market operations as necessary to maintain the federal funds rate in a target range of 0.00 to 0.25 percent. •Increase the System Open Market Account holdings of Treasury securities, agency mortgage-backed securities (MBS), and agency commercial mortgage-backed securities (CMBS) in the amounts needed to support the smooth functioning of markets for these securities. •Conduct term and overnight repurchase agreement operations to support effective policy implementation and the smooth functioning of short-term U.S. dollar funding markets. •Conduct overnight reverse repurchase agreement operations at an offering rate of 0.00 percent and with a per-counterparty limit of $30 billion per day; the per-counterparty limit can be temporarily increased at the discretion of the Chair. •Roll over at auction all principal payments from the Federal Reserve's holdings of Treasury securities and reinvest all principal payments from the Federal Reserve's holdings of agency debt and agency MBS in agency MBS and all principal payments from holdings of agency CMBS in agency CMBS. •Engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve's agency MBS transactions."

Updates on 30 April 2020 Federal Reserve issues FOMC statement: released at 2:00 p.m. EDT, 29 April 2020 Extracts: The ongoing public health crisis will weigh heavily on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term. In light of these developments, the Committee decided to maintain the target range for the federal funds rate at 0 to 0.25 percent. The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals. To support the flow of credit to households and businesses, the Federal Reserve will continue to purchase Treasury securities and agency residential and commercial mortgage-backed securities in the amounts needed to support smooth market functioning, thereby fostering effective transmission of monetary policy to broader financial conditions. In addition, the Open Market Desk will continue to offer large-scale overnight and term repurchase agreement operations. The Committee will closely monitor market conditions and is prepared to adjust its plans as appropriate.

Updates on 16 March 2020 Federal Reserve issues FOMC statement dated 15 March 2020, 5:00 p.m. EDT (Audio) Extracts: Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The effects of the coronavirus will weigh on economic activity in the near term and pose risks to the economic outlook. In light of these developments, the Committee decided to lower the target range for the federal funds rate to 0.00 to 0.25 percent. The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals. This action will help support economic activity, strong labor market conditions, and inflation returning to the Committee's symmetric 2 percent objective.

Updates on 5 March 2020 Federal Reserve issues FOMC statement dated 3 March 2020 (EDT) (video) Extracts: The fundamentals of the U.S. economy remain strong. However, the coronavirus poses evolving risks to economic activity. In light of these risks and in support of achieving its maximum employment and price stability goals, the Federal Open Market Committee decided today to lower the target range for the federal funds rate by 0.5 percentage point, to 1.00 to 1.25 %. The Committee is closely monitoring developments and their implications for the economic outlook and will use its tools and act as appropriate to support the economy.

Updates on 20 February 2020: Minutes of the Federal Open Market Committee dated January 28-29, 2020 (published on 19 February EDT) Extracts: At the conclusion of the discussion, the Committee voted to authorize and direct the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the SOMA in accordance with the following domestic policy directive, for release at 2:00 p.m.: "Effective January 30, 2020, the Federal Open Market Committee directs the Desk to undertake open market operations as necessary to maintain the federal funds rate in a target range of 1.50 to 1.75 percent. In light of recent and expected increases in the Federal Reserve's non-reserve liabilities, the Committee directs the Desk to continue purchasing Treasury bills at least into the second quarter of 2020 to maintain over time ample reserve balances at or above the level that prevailed in early September 2019. The Committee also directs the Desk to continue conducting term and overnight repurchase agreement operations at least through April 2020 to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation. In addition, the Committee directs the Desk to conduct overnight reverse repurchase operations (and reverse repurchase operations with maturities of more than one day when necessary to accommodate weekend, holiday, or similar trading conventions) at an offering rate of 1.50 percent, in amounts limited only by the value of Treasury securities held outright in the System Open Market Account that are available for such operations and by a per-counterparty limit of $30 billion per day.

The Committee directs the Desk to continue rolling over at auction all principal payments from the Federal Reserve's holdings of Treasury securities and to continue reinvesting all principal payments from the Federal Reserve's holdings of agency debt and agency mortgage-backed securities received during each calendar month. Principal payments from agency debt and agency mortgage-backed securities up to $20 billion per month will continue to be reinvested in Treasury securities to roughly match the maturity composition of Treasury securities outstanding; principal payments in excess of $20 billion per month will continue to be reinvested in agency mortgage-backed securities. Small deviations from these amounts for operational reasons are acceptable.

The Committee also directs the Desk to engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve's agency mortgage-backed securities transactions."

The vote also encompassed approval of the statement below for release at 2:00 p.m.: "Information received since the Federal Open Market Committee met in December indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending has been rising at a moderate pace, business fixed investment and exports remain weak. On a 12‑month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee decided to maintain the target range for the federal funds rate at 1.50 to 1.75 percent. The Committee judges that the current stance of monetary policy is appropriate to support sustained expansion of economic activity, strong labor market conditions, and inflation returning to the Committee's symmetric 2 percent objective. The Committee will continue to monitor the implications of incoming information for the economic outlook, including global developments and muted inflation pressures, as it assesses the appropriate path of the target range for the federal funds rate.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2% inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments."

Updates on 12 February 2020 Semiannual Monetary Policy Report to the Congress by Chair Jerome H. Powell (Published on 11 February 2020 EST) Extracts: The current low interest rate environment also means that it would be important for fiscal policy to help support the economy if it weakens. Putting the federal budget on a sustainable path when the economy is strong would help ensure that policymakers have the space to use fiscal policy to assist in stabilizing the economy during a downturn. A more sustainable federal budget could also support the economy's growth over the long term.

Finally, I will briefly review our planned technical operations to implement monetary policy. The February Monetary Policy Report provides details of our operations to date. Last October, the FOMC announced a plan to purchase Treasury bills and conduct repo operations. These actions have been successful in providing an ample supply of reserves to the banking system and effective control of the federal funds rate. As our bill purchases continue to build reserves toward levels that maintain ample conditions, we intend to gradually transition away from the active use of repo operations. Also, as reserves reach durably ample levels, we intend to slow our purchases to a pace that will allow our balance sheet to grow in line with trend demand for our liabilities. All of these technical measures support the efficient and effective implementation of monetary policy. They are not intended to represent a change in the stance of monetary policy. As always, we stand ready to adjust the details of our technical operations as conditions warrant.

Updates on 8 February 2020 Federal Reserve Board releases hypothetical scenarios for 2020 Stress Test Exercises (Published on 6 February 2020, 4:30pm EST)

Updates on 30 January 2020 Federal Reserve issues FOMC statement dated 29 January 2020, 2:00pm EST Extracts: The Committee decided to maintain the target range for the federal funds rate at 1.50 to 1.75 percent. In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Implementation Note issued January 29, 2020, 2:00pm EST Extracts: In addition, the Committee directs the Desk to conduct overnight reverse repurchase operations (and reverse repurchase operations with maturities of more than one day when necessary to accommodate weekend, holiday, or similar trading conventions) at an offering rate of 1.50 percent, in amounts limited only by the value of Treasury securities held outright in the System Open Market Account that are available for such operations and by a per-counterparty limit of $30 billion per day. Principal payments from agency debt and agency mortgage-backed securities up to $20 billion per month will continue to be reinvested in Treasury securities to roughly match the maturity composition of Treasury securities outstanding; principal payments in excess of $20 billion per month will continue to be reinvested in agency mortgage-backed securities. Small deviations from these amounts for operational reasons are acceptable.

Press Conference Transcript (released on 29 January 2020, 2:00pm EST)

Updates on 4 January 2020: Minutes of the Federal Open Market Committee dated December 10–11, 2019 (Published on 4 January 2019, SGT) Extracts: Real residential investment appeared to be increasing further after rising solidly in the third quarter. Both starts and building permit issuance for single-family homes increased in October, and starts of multifamily units also rose. Existing home sales continued to increase in October, although new home sales edged down following a solid gain in the third quarter. All told, the data on construction and sales continued to suggest that the decline in mortgage rates since late 2018 has been boosting housing activity.

Real non-residential private fixed investment remained weak overall after declining in the second and third quarters. Nominal shipments and new orders of nondefense capital goods excluding aircraft increased solidly in October following a string of decreases, although many forward-looking indicators pointed to continued softness in business equipment spending. Most measures of business sentiment were still downbeat, analysts' expectations of firms' longer-term profit growth edged down further, and concerns about trade developments continued to weigh on firms' investment decisions. Nominal business expenditures for non-residential structures outside of the drilling and mining sector continued to decline in October, and the total number of crude oil and natural gas rigs in operation—an indicator of business spending for structures in the drilling and mining sector—fell further through early December.

Financing conditions in the residential mortgage market remained accommodative over the intermeeting period. Mortgage rates were little changed since the October FOMC meeting. Consistent with this year's decline in mortgage rates, home-purchase originations and refinancing originations both rose. Mortgage credit standards were little changed.

Financing conditions in consumer credit markets remained generally supportive of growth in consumer spending, although conditions continued to be tight for nonprime borrowers. Auto loans increased, consistent with significant declines in auto loan interest rates this year. Credit card debt grew at a solid pace, and interest rates on credit card debt began to fall. Consumer asset‑backed securities issuance was strong through October as spreads stabilized at levels that were somewhat above their post-crisis averages.

"Effective December 12, 2019, the Federal Open Market Committee directs the Desk to undertake open market operations as necessary to maintain the federal funds rate in a target range of 1.5 to 1.75 percent. In light of recent and expected increases in the Federal Reserve's non-reserve liabilities, the Committee directs the Desk to continue purchasing Treasury bills at least into the second quarter of 2020 to maintain over time ample reserve balances at or above the level that prevailed in early September 2019. The Committee also directs the Desk to continue conducting term and overnight repurchase agreement operations at least through January 2020 to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation. In addition, the Committee directs the Desk to conduct overnight reverse repurchase operations (and reverse repurchase operations with maturities of more than one day when necessary to accommodate weekend, holiday, or similar trading conventions) at an offering rate of 1.45 percent, in amounts limited only by the value of Treasury securities held outright in the System Open Market Account that are available for such operations and by a per-counterparty limit of $30 billion per day.

The Committee directs the Desk to continue rolling over at auction all principal payments from the Federal Reserve's holdings of Treasury securities and to continue reinvesting all principal payments from the Federal Reserve's holdings of agency debt and agency mortgage-backed securities received during each calendar month. Principal payments from agency debt and agency mortgage-backed securities up to $20 billion per month will continue to be reinvested in Treasury securities to roughly match the maturity composition of Treasury securities outstanding; principal payments in excess of $20 billion per month will continue to be reinvested in agency mortgage-backed securities. Small deviations from these amounts for operational reasons are acceptable.

The Committee also directs the Desk to engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve's agency mortgage-backed securities transactions."

Updates on 12 December 2019 Federal Reserve issues FOMC statement from the December 10-11 FOMC Meeting Extracts: On a 12 month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee decided to maintain the target range for the federal funds rate at 1.5% to 1.75%. The Committee judges that the current stance of monetary policy is appropriate to support sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee's symmetric 2 percent objective. The Committee will continue to monitor the implications of incoming information for the economic outlook, including global developments and muted inflation pressures, as it assesses the appropriate path of the target range for the federal funds rate.

Federal Reserve Board and FOMC release economic projections from the December 10-11 FOMC meeting

Updates on 27 November 2019 Federal Reserve: Speech by Chair Jerome H. Powell “Building on the Gains from the Long Expansion” (dated 25 November 2019 EDT) Extracts: In August, the Bureau of Labor Statistics previewed a likely revision to its count of payroll job creation for the 12 months ended March 2019. The preview indicated that job gains over that period were about half a million lower than previously reported. On a monthly basis, job gains were likely about 170,000 per month, rather than 210,000. While this news did not dramatically alter our outlook, it pointed to an economy with somewhat less momentum than we had thought.3

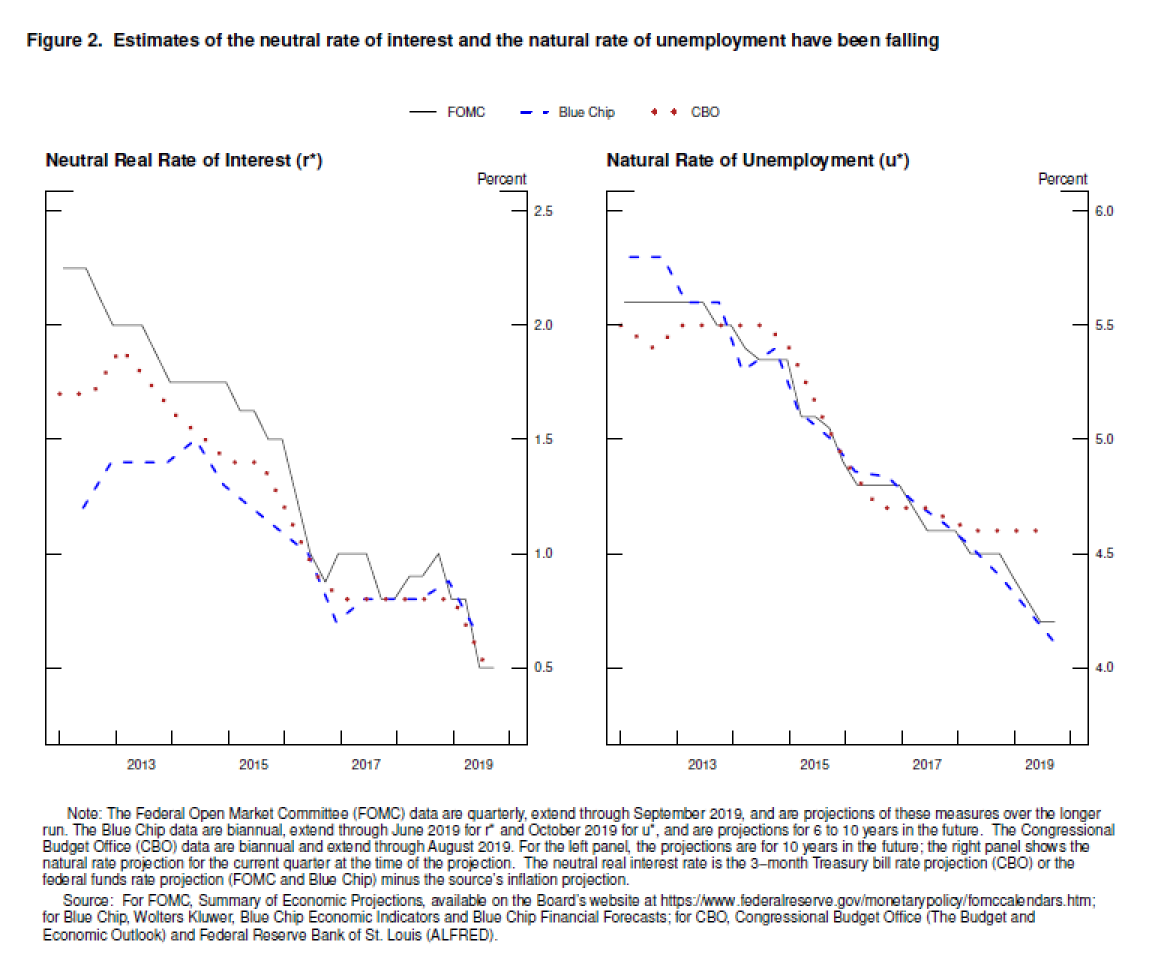

Uncertainty about how our policies are affecting the economy also entered our discussions. As you know, we set our policy interest rate to achieve our goals of maximum employment and stable prices. In doing so, we often refer to certain benchmarks. One of these is the interest rate that would be neutral—neither restraining the economy nor pushing it upward. We call that rate "r*" (pronounced "r star"). A policy rate above r* would tend to restrain economic activity, while a setting below r* would tend to speed up the economy. A second benchmark is the natural rate of unemployment, which is the lowest rate of unemployment that would not create upward pressure on inflation. We call that rate "u*" (pronounced "u star"). You can think of r* and u* as two of the main stars by which we navigate. In an ideal world, policymakers could rely on these stars like mariners before the advent of GPS. But, unlike celestial stars on a clear night, we cannot directly observe these stars, and their values change in ways that are difficult to track in real time. Standard estimates of r* and u* made by policymakers and other analysts have been falling since 2012 (figure 2). Since the end of last year, incoming data—especially muted inflation data—prompted analysts inside and outside the Fed to again revise down their estimates of r* and u*.4 Taken at face value, a lower r* would suggest that monetary policy is providing somewhat less support for employment and inflation than previously believed, and the fall in u* would suggest that the labor market was less tight than believed.5 Both could help explain the weakness in inflation. As with the revised jobs data, these revised estimates of the stars were not a game changer for policy, but they provided another reason why a somewhat lower setting of our policy interest rate might be appropriate.

How did we add up all of these considerations? To help keep the U.S. economy strong in the face of global developments and to provide some insurance against ongoing risks, we progressively eased the stance of monetary policy over the course of the year. First, we signaled that increases in our short-term interest rate were unlikely. Then, from July to October, we reduced the target range for the federal funds rate by 3/4 percentage point. The full effects of these monetary policy actions will be felt over time, but we believe they are already helping to support consumer and business sentiment and boosting spending in interest-sensitive sectors, such as housing and consumer durable goods.

We see the current stance of monetary policy as likely to remain appropriate as long as incoming information about the economy remains broadly consistent with our outlook of moderate economic growth, a strong labor market, and inflation near our symmetric 2 percent objective. Looking ahead, we will be monitoring the effects of our policy actions, along with other information bearing on the outlook, as we assess the appropriate path of the target range for the federal funds rate. Of course, if developments emerge that cause a material reassessment of our outlook, we would respond accordingly. Policy is not on a preset course.

Updates on 21 November 2019 FOMC Minutes for 29-30 October 2019 (published on 20 November 2019, 2pm EDT)

With effective from October 31, 2019, FOMC will maintain the federal funds rate in a target range of 1.5% to 1.75% percent. FOMC decided to purchase Treasury bills at least into the second quarter of next year to maintain over time ample reserve balances at or above the level that prevailed in early September 2019. FOMC will conduct term and overnight repurchase agreement operations at least through January of next year to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation. In addition, FOMC will conduct overnight reverse repurchase operations (and reverse repurchase operations with maturities of more than one day when necessary to accommodate weekend, holiday, or similar trading conventions) at an offering rate of 1.45%, in amounts limited only by the value of Treasury securities held outright in the System Open Market Account that are available for such operations and by a per-counterparty limit of $30 billion per day.

FOMC will continue rolling over at auction all principal payments from the Federal Reserve's holdings of Treasury securities and to continue reinvesting all principal payments from the Federal Reserve's holdings of agency debt and agency mortgage-backed securities received during each calendar month. Principal payments from agency debt and agency mortgage-backed securities up to $20 billion per month will continue to be reinvested in Treasury securities to roughly match the maturity composition of Treasury securities outstanding; principal payments in excess of $20 billion per month will continue to be reinvested in agency mortgage-backed securities. Small deviations from these amounts for operational reasons are acceptable.

FOMC will engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve's agency mortgage-backed securities transactions.

In determining the timing and size of future adjustments to the target range for the federal funds rate, FOMC will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2% inflation objective. This assessment will take into account a wide range of information, includin measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Click “Next” below for more past records.

|

{kind=link}